Spring Forward (Guidance)

All that fun for nothing?! The FOMC succeeded in delivering a nothingburger on March 20th and effectively kicked the monetary policy can down the road to the June meeting. In the days following that meeting, Fed speakers have been at pains to push back on the need to cut at all, and certainly not anytime soon. But perhaps most concerning is the lack of agreement on exactly where the neutral rate is these days. In fact, there hasn’t been much mention of r* in the past few months and the estimates published by the Federal Reserve Bank of New York are published with a relatively long lag, so the most recent observation only runs through October 2023. Those estimates from the Laubach-Williams and Holston-Laubach-Williams models actually show a pretty substantial decline in the estimated neutral rate since peaking in late 2021. There has been plenty of speculation that a potential productivity boom sparked by widespread adoption of AI could increase the neutral rate in future years, but the reality is that demographics tend to have a larger impact on r* and the widespread adoption of the internet in the years following Y2K actually did very little to arrest the decline of total factor productivity in the post-WWII period. There was an uptick during the 1990’s, but that was well before most businesses demostrated wide-spread internet adoption (the 90’s was mostly about the growth in personal computer use).

I have tended to give the Fed pretty good marks for their efforts over the past decade, but I worry that Jerome Powell the lawyer, and not Jerome Powell the central banker is now in charge - having steered the Fed away from providing much forward guidance and running policy by spending all their time and energy looking backwards. That is not a problem for today, as the growth and inflation mix is quite favorable at the moment, but it certainly could become a problem if growth and the labor market were to slow and the Fed was continuing to fight the last war (in this case, inflation). Again, the Fed has the luxury of being able to continue to talk tough on inflation at the moment, but frankly, not much has changed in the data over the past quarter. If anything, the growth outlook is, at the margin, maybe even a bit better. China manufacturing activity is showing a glimmer of an uptick, if only because exports have been strong. The “big bang” fiscal stimulus that many are hoping for may disappoint, but the economy has not been a disaster either. Likewise in Japan and Europe. The macro data to start 2024 may be boring, but sometimes boring is OK.

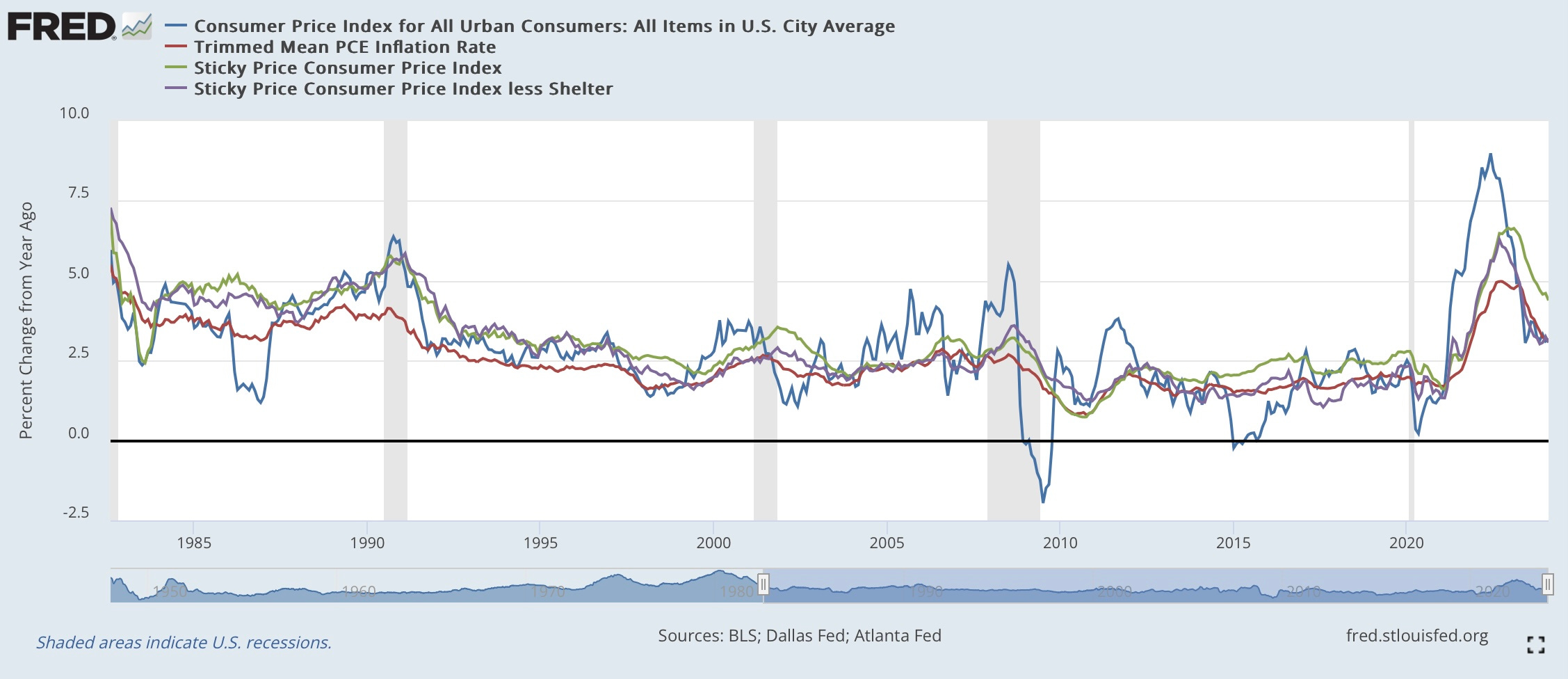

The continued obsession with inflation is starting to get old. The dirty little secret in economics is that like productivity, nobody knows much about what drives inflation dynamics. Three years on from the “transitory” era and we are still debating the balance of attribution between supply shocks and demand drivers of the inflation surge. The reality is that inflation is returning nicely back toward targets and while it may not be a smooth ride back to 2%, given the blunt instruments at the disposal of monetary authorities, it will be close enough for government work. Given the historical volatility in inflation, we are at least now withing rounding error of “normal”. [see chart below]

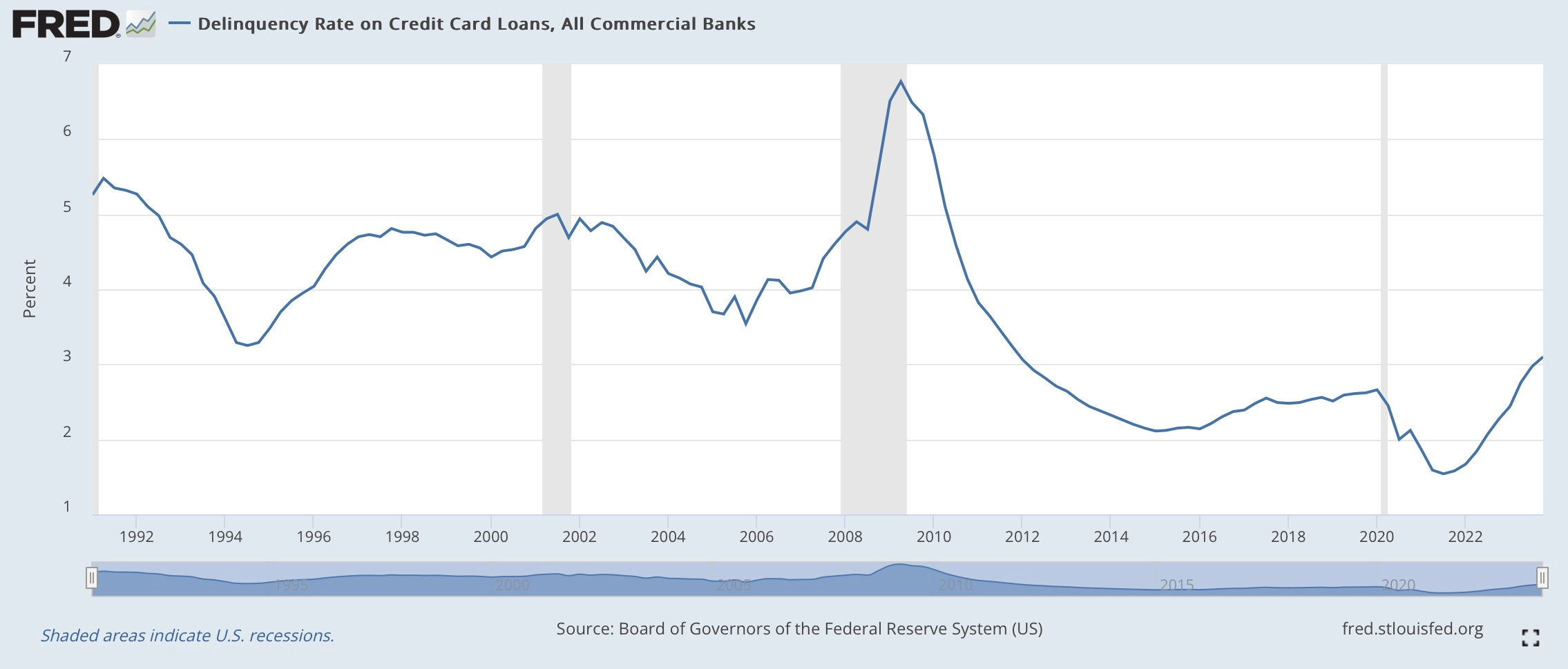

Another glimmer of hope came from the early-February release of the Fed’s quarterly Senior Loan Officer Survey which showed a significant tick down in the net percentage of banks tightening lending conditions. And to go along with that data, it appears as though the total growth in the nominal dollar volume of commercial and industrial loans outstanding has arrested its decline. That is not to say that the banking system is completely out of the woods yet, as commercial real estate may yet be a burden as we progress through the year, but the evidence from credit markets so far is that the rest of the real economy is holding up just fine. I will admit that I had my doubts 3-6 months ago based on the pace of rundown in “excess savings”, but despite an uptick in credit card deliquencies, households still seem like they are in decent shape relative to history. [see next exhibit]

Finally, while we may actually get the “immaculate disinflation” and soft landing similar to the experience of the late ‘90s, that is not to say that the time is right to be wildly bullish on equities. It is still a concern that sentiment and valuation are both in the highest quintiles - but both of these important indicators can remain frothy for much longer than anyone expects and they are both better buy signals at the other extreme than they are sell signals. The good news is that while the Fed remains reluctant to cut, there are still attractive yields to be harvested at the short end of the yeild curve and duration will again protect on the downside if the economy were to show signs of weakness. The reports of the death of the 60/40 balanced portfolio were wildly exaggerated.